I still remember my very first credit card was actually a supplementary card from my sister. The credit limit at the time was only RM1,000. That was somewhere in 2003. It was long time ago. Indeed. After using credit card for almost two decades, I realised that there are many advantages to the credit card.

First, credit card builds you credit score and debit cards don’t. The better the credit score, the easier for you to buy a car or a house in the future. Banks rely on the information contained within Central Credit Reference Information System (CCRIS) to assess your creditworthiness for reliability in paying money back in the past. If you pay any outstanding balance before the due date every month, then your credit score will increase thus easier to obtain financing from the banks.

Discover more topics via spotify.Second, by using credit card, you are spending bank’s money instead of your own savings, hence your money is sitting in the bank safely and not expose to anyone to find it. In the event of someone uses your cards fraudulently, you will have zero liability of that charges. Your savings are still sitting in the bank as the loss is bank’s money. Any investigation that take weeks or months will not affect your own savings. In short, if you use your debit card, you are exposing your money to the world; if you use credit card you are spending on bank’s money.

However, with so many advantages of using credit card, it is still associate with a deadly underlying risk that most people not aware - credit card makes you spend more!

The first principle is that you must not fool yourself and you are the easiest person to fool. -Richard Feynman

With the concept of spending future’s money instead of your own savings, it tend to make people take it lightly and spend without thinking twice. It makes you feel more relax and less vigilant about over-spending as you believe the ‘future’ you can settle the payment. Credit card also come with another evil feature - minimal payment, it allows people to pay minimal amount by charging certain interest. And because it further extend the flexibility of payment mode, some people willing to pay in minimal in exchange of greater spending power. Last but not least, credit card have instalment plan too. It allow people to buy something they are supposedly not capable to, however, through instalment plan, they now can afford it.

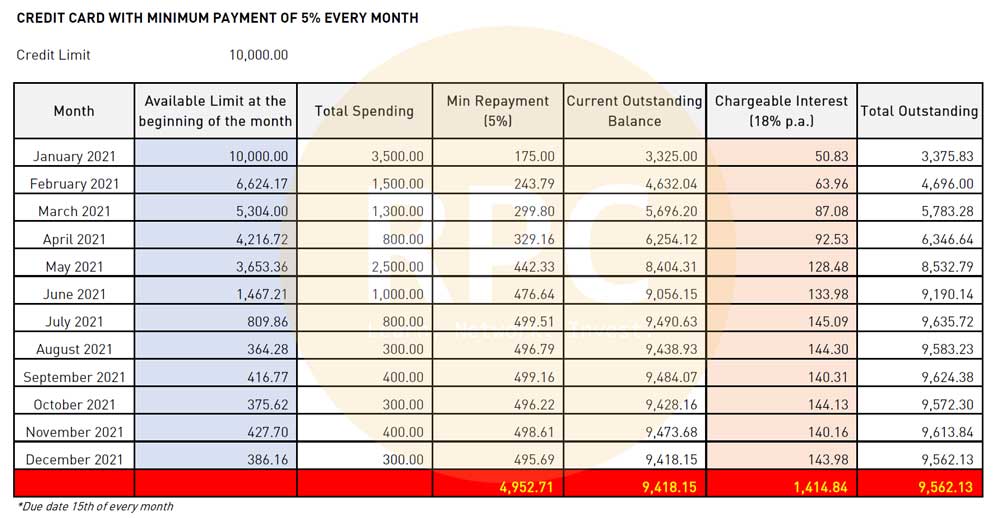

The schedule below shows a minimum payment of 5% every month on total outstanding balance with continual spending on the credit card over 12 months period. If you continue to use the card and not clearing the outstanding balance, then you are literally building up debt. You are paying unnecessary interest of RM1.4k over the 12 months for nothing. In addition, the table shows clearly if you pay minimum every month, not only you will not be able to clear any outstanding but it’s the opposite with increasing debt!

This will further burden your future financial ability and by continue using all the feature of credit cards, it tends to make people hardly know their real financial position, unless you are very good in finances. Some people also believe to pay the credit card bill at the last day in order to maximize its benefit and flexibility. However, what people don’t understand is- if you pay at the last day of the bill, your additional days of savings won’t make you wealthy interest, but if you accidentally overdue your bill, the penalty will be very substantial as compare to your savings’ interest.

Paying at the last day also make you have the least flexibility. If you always stretch yourself to the maximum,you will find it hard to turnaround especially during emergency or any unforeseen things to happen. Stretching your finances means you are taking away your flexibility in terms of time for adjustment or fund allocation. You will then realise you have no time because you have already stretched to the max.

So, shall we use credit card?

Credit card has its pros and cons as above-mentioned. The key is to understand the psychology of spending and learn how to plan your finances well. Credit card itself is not bad, but if the person who uses it has no self-discipline, have bad spending behaviour and equip with very little financial knowledge, then the credit card may ruin someone’s life. So the goal is not about credit card, it’s about how to equip yourself with more knowledge and have clear objective in using any tools.

「If this article is useful to you, feel free to buy me a coffee ☕」

Danny KO @ RPC

Danny KO @ RPC

If this article is useful to you, feel free to buy me a coffee ☕