Let’s start with a big claim: I believe that the 18-year property cycle is one of the most powerful concepts you can know about as a property investor. That is why understanding the 18 year property cycle in Malaysia is very important.

CHECK OUT MY BOOK

My book was written in 2014 and published in early 2015. When this book was published, Malaysia 18-year property cycle based on the data collected in Malaysia, has not reached its full cycle. However, true to its clock the time is in tandem with the cycle in my book till to date. To me this is a very useful guide to the 18-year property cycles in Malaysia which can be projected into the future too.

Why the 18-year property cycle? Because once you understand the property cycle, you’ll know:

- That there’s a reason why property prices always go up in the long run – giving you more confidence that they will continue to do so.

- That they won’t go up in a nice smooth, straight line: crashes along the way are inevitable because of the way the system is set up.

- That you can ignore what the newspapers say about property prices and market outlook of the future, and have a far better understanding of what’s likely to happen next by looking for certain signals in the world around you.

In short, a lot of facets of property investment that seem random or uncertain will suddenly make a lot more sense.

With this knowledge you can at least avoid making the wrong move at the wrong time that would put your investments portfolio in jeopardy – and at most, you can make it a central pillar of your investment strategy.

You could just take my word for it when I say that property is cyclical – but you won’t be convinced enough to take action based on it until you’ve fully grasped the logic for yourself.

So we’ll get to talking about how you can use the 18-year property cycle to make better investment decisions – but first, we need to get into the economics that underpin it…

WHY IS THERE A PROPERTY CYCLE?

In pretty much every market other than land – whether it’s goods like cars, or labour like hairdressers – the forces of supply and demand keep prices roughly in balance.

If we all become more greedy and start buying more and more of a product, it will be impossible to meet the up surged in demand and vendors will raise their prices to profit from those desperate enough to pay more for their coiffure.

See also Where Are We In The Real Estate Cycle 2020

Soon, these higher prices will attract new and more competitors into the market, and the extra supply will mean that everyone has to reduce their prices to remain competitive.

As seen in this simple economic term – Ricardo Law of Rent, supply and demand work in tandem to keep prices stable over time.

In the real estate market though, this can’t happen because the amount of land supply in existence is fixed: you can’t just magic up a load of extra land if demand for it goes up. (Yes, you could relax planning restrictions, and in any case, demand is normally concentrated around established locations. Of course you may reclaimed more land from the sea over a time too)

As a result, when the economy is growing and there’s demand for new homes, shops and factories, that extra demand will push prices up. And because there’s no supply mechanism to pull prices back down, land prices increase faster than wages and the price of goods.

It doesn’t take people long to realise what’s happening and see that they’ll get the best return on their money if they put it into property (as a proxy for land). At times of particularly high demand, people “speculate” by buying property on the assumption that the price will continue to go up. In Malaysia, this scenario if no different from other developed countries.

Because property prices increase faster than wages do, property eventually becomes unaffordable for the majority of people. When this happens, the bust comes: property prices plummet over a period, causing chaos for the banks (which have been lending money secured against high-priced property). The banks will then tighten lending, basically to also protect their past portfolios to ensure businesses will not shut down – which all have obvious knock-on affects the stock markets, retail and employment levels and others.

Eventually of course, prices drop to a more sustainable level and everything gradually goes back to normal – at which point the whole cycle starts again.

Importantly, each cycle starts from a higher “bottom” than the previous one – so the long-term trend is always upwards, even though there’s a lot of volatility along the way.

That, in a nutshell, is the property cycle. It would be more accurate to call it “the land cycle”, because the cost of building a house on a piece of land is much the same in KL as it is in smaller towns, and won’t cost more over the short period/years than it does today. But house prices are more accessible to us than land prices, so we can “read” property prices to tell us what’s happening in the land market – and therefore what’s ahead for the wider economy.

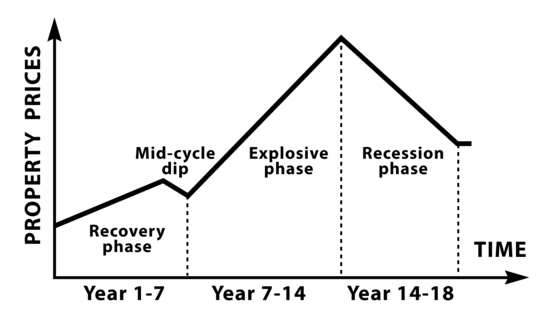

THE STAGES OF THE 18-YEAR PROPERTY CYCLE

Various economists like Homer Hoyt,Roz Wenzlizk ,Fred Harrison from UK, Phillip J Anderson (Phil Anderson) from US are among the first few people to identify the existence of the 18-year property cycle. They traced it back for hundreds of years to conclude that the length of a full cycle averages out to 18 years, with each cycle divided into distinct stages.

Chances are you’ll have a memory of some property cycle – possibly more. As we talk about the indicators that signify each stage, you’ll probably be able to think back to the clues that were there, in retrospect, in cycles you’ve experienced in the past.

This is critical because if you don’t look for your own evidence, the media will lead you astray. PREDICTIONS ON 31st DEC 2015

As we’ll see, at every stage, the professionals who are watching the signals act very differently from the amateurs who are watching the media – and they get far better results.

So, let’s take a look at each stage of the cycle, what drives the shift from one stage to the next, and what different types of investors are thinking and doing at each point…

- We’ll start as prices have bottomed out at the end of the recession, and the recovery phase is just beginning to get underway. Prices have fallen far enough to tempt the bravest investors back into the market, attracted by the high yields that are on offer as a result of prices falling while rents stay pretty much the same. (Rents don’t fall drastically because everyone still needs somewhere to live. Even if renters were brave enough to take advantage of the lower prices and buy, this is the toughest point in the cycle at which to get a mortgage because banks are struggling too.)These brave investors are what we can think of as the “smart money”: contrarian investors who’ve spotted the opportunity to get in at rock bottom, and are willing to take the risk of buying up assets while confidence is low and the investment case is still unproven. Of course, nobody knows precisely at what point the bottom of the market has been reached.

Smart investors are just willing to take an educated guess, based on the knowledge that their upside potential is greater than their downside risk. Meanwhile, amateur investors are totally absent from the market – even though lower prices and lack of competition mean that it’s precisely the best time to buy. They might even crystallise their losses by selling at the bottom of the cycle “before prices fall any further”, or be forced to sell because their portfolio was poorly structured to weather a recession or for some unforeseen family crisis. So, if there’s pessimism all around you and the media is full of doom and gloom even though the major catastrophic events of the recession seem to be over, the recovery phase might just be getting underway.

It is also during this gloomy period that the government will try to boost the property market. Weeks before Budget 2017 was tabled, Prime Minister Datuk Seri Najib Razak launched an online survey where Malaysians were asked to list their top three concerns about the economy. In pole position were the rising cost of living and soaring housing prices. This lead to the introduction of Prima Housing which helps sustains the property market in 2016 and 2017.

In retrospective, during the Asian Financial Crisis, various economic and tax cuts-tax, low barriers to home ownership with introduction of zero lock in period, exemptions of stamp duty, 100% financing etc were also introduced.

-

As the initial recovery phase develops, buyers are still very cautious and uncertain of the markets until more buyers will have the confidence to enter the market – having the effect of pushing prices gradually upwards. Look out for big companies and pension funds starting to buy up distressed portfolios: they have the market intelligence to get in early but can’t take the risk of getting in too early, so it’s a good signal of the recovery solidifying. The prime assets will always be the most attractive, so this early growth tends to begin in the centres of the most economically powerful cities and “ripple out” from there.

-

Perhaps following the more optimistic market, there will be a slight mid-cycle dip as the earliest movers take their profits. Thereafter, the recovery phase will give way to the explosive phase. It’s now clear that prices are on the up, and the banks will be over the shock and willing to start lending again. That supplies enough confidence and capital for major building projects to start again, so expect to see more cranes on the skyline. House prices will begin to increase markedly faster than wages, and it’s at this point that the media gets interested – you’ll probably start to see headlines along the lines of “House prices increasing beyond affordability of homeowners” and “ Long queue at property launches”. Fuelled by this, people start to speculate: they either “move up the ladder” to somewhere bigger before it gets even further out of their reach, or they increase the mortgage against their home to fund holidays and cars.

Banks make it easy for them to do so, because everything’s in full swing and they just want to lend as much as they can. At some point, logic and fundamentals go out the window and group psychology kicks in. The higher prices go, the more everyone assumes that prices will keep going up – so they buy at any level, pushing prices even further. The smart investors who got in early will be quietly selling off their holdings to lock in their profits, but the mania is such that nobody will notice. As we move towards the peak of the explosive phase, it’s a seller’s market, and sellers know it – so estate agents conduct “open house”-style block viewings, pre-launch at developers’ sales office for regsitrants to stoke demand even further. Even properties that wouldn’t have excited anyone a few years earlier were all bought up. Properties routinely sell for well above their asking price, and developers start marketing ever more new launches to capitalise on the demand.

Banks aren’t immune to the mania, so they loosen their lending criteria to grab a bigger piece of the action. Even if some individuals within the banks are aware that the boom is unsustainable, they’re still under pressure to compete with everyone else: shareholders won’t be happy with them sitting back and not lending while everyone else is so optimistic.

This lax credit keeps the party going for longer than anyone would previously have expected. At some point, a commentator or economist will predict that everything’s about to come crashing down because everything is so fundamentally overvalued – but a year later prices will still be rising, and that commentator will be branded a “doom-monger”.

-

The final couple of years of the explosive phase, as prices and mania reach their peak, are what Fred Harrison branded the “winner’s curse” phase. Why is it a curse to be a “winner” by placing the highest bid for a property during this time? Because the next recession isn’t far away, and it won’t be long before the asset you’ve bought will be worth markedly less.You obviously can’t know when the “final years” of the upswing are until they’ve already happened and it’s too late, but there’s no shortage of warning signs that we may be near the top if you know where to look. One such sign is the announcement of overblown building projects like “world’s tallest building”, and other sorts of over-ambitious ideas. These projects are conceived at a time of supreme confidence and funded in a permissive lending environment. It’s often the case that the bust has already happened by the time they’re completed, and they sit mostly empty – a monument to the delusion that has just passed. Another surefire sign is the rationalising of the ridiculously high prices that the mania has brought about. Justifications will be found for why “things are different this time” and we’re in for an era of permanently higher prices… yet at some point reality will set in, and the recession phase is imminent.

-

Because the market was being driven by sentiment rather than fundamentals in the frothiest years, it’s easy for confidence to suddenly evaporate and take the market with it. Prices plummet, and people who are over-leveraged go a bankrupt – triggering wave of forced selling, which pushes prices down even further. It’s impossible to pinpoint the exact moment when this is going to happen, but you won’t need to be told when it does: nothing sells newspapers like bad news, so the media will stoke the panic with endless horror stories. The recession phase seems like it will last forever, but it never does: at some point the smart money will be tempted back in, and the whole thing can start all over again. Check out more about the 18 years cycle via Property Millionaires’ Secret Clock webpage

「If this article is useful to you, feel free to buy me a coffee ☕」

Danny KO @ RPC

Danny KO @ RPC

If this article is useful to you, feel free to buy me a coffee ☕